If you‘ve attempted to access your EPF account in the recent past and you‘ve gotten a blank passbook, received a ‘service unavailable’ message or seen the portal suddenly appear unfamiliar, you don‘t have hallucinations the EPFO quietly re-worked a very large portion of its backend this year and the transition hasn‘t been smooth for all.

Almost all the articles showing the ‘what‘s new’ for employees provident fund organisation end with a list of the new features and nothing else. Which isn‘t going to get you to withdraw money, view your interest credit or work out if your employer has added you correctly. This article explains what is truly different, where the pain points are and how to avoid them whether you‘re an employee tracking your own account or running payroll for a small team.

Table of Contents

The Employees Provident Fund Organisation Updates Nobody Explained Properly

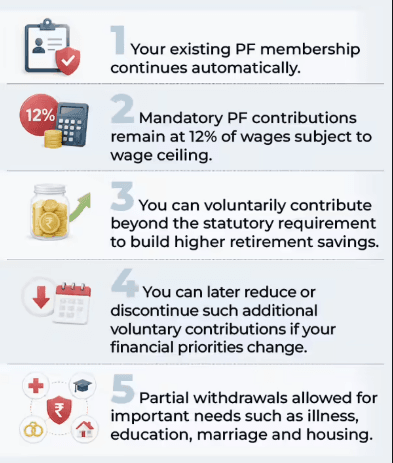

Conclusion short: effective from 1 July 2026 the EPF Scheme, 2026 superseded the pension scheme 1952 of 1 July 1952. That rings a bit of a change, which may sound as intimidating as ‘substituting’ for cancelled. But for most subscribers the nitty gritties (contribution rates, access limits, core rules) have not been significantly altered; and what has changed is the legal envelope, bringing it into conformity with the Code on Social Security, 2020; and enshrining digital innovations such as e-claims and e-inspections as part of the text of the scheme.

The rate was left unchanged at 8.25% for FY 25–26, the same as the previous few years. So if you were expecting a cut or a hike the period has been flat, nothing there. The new item is the limit on exempted PF trusts can‘t report more than 2% above the govt rate, which limits them to about 10.25% for this year.

That‘s not the real story, though. The real story is what lies under it all.

EPFO 3.0: The Shift That Actually Matters

For many years, EPFO maintained separate regional databases that didn‘t communicate effectively. Moving between state borders with your employer meant your PF account histories were spread out and finding a 40 year old account meant walking into an office.

EPFO 3.0 is based on a project called CITES (Central Initiated Transfer of ESI and pension payments) – a single centralised database that will do away with the previous region-by-region system. It will also replace this with a unified member portal, automated transfers to Aadhaar-mapped UANs, partial withdrawals based on UPI, and life certificates for pensioners via facial recognition without the need to visit the office.

Put simply: EPFO organized “twenty regional offices with their own records” to “one [single IT system] that‘s supposed to know everything about you.” A laudable goal for something as important as your employees provident fund balance. But it is not very surprising then, that migrations of that scale are almost never flawless on the first try and this one was no exception.

I Checked My EPF Passbook After the CITES Migration — Here’s What I Found

A few days after the centralized portal went live I managed to get at my own passbook, almost just to see what the ‘click-of-a-button’ transition was really like. It was OK, the passbook loaded quickly and the balance was as I thought it should be, but the portal was very sluggish and an old job didn‘t show up under Service History until I checked a second time, a few days later.

So a small thing, but it informs you of something: the data is present, it just perhaps isn‘t displaying consistently at this point. If your passbook appears partial at this point in time, it doesn‘t necessarily mean your documentation has gone missing, but rather that the migration has yet to sync your record. Perhaps worth re-checking before you throw your hands up or calls down the grievance.

Where This Still Breaks (And Why It’s Not Your Fault)

A few pain points show up repeatedly across employee and employer complaints right now:

- Unlinked or orphaned UANs that sat around from the old regional database days for individuals who worked in several states.

- The Passbook and the portal outage both happened just before or after the interest-credit cycle and the CITES rollout.

- Theinconsistent user experience on main EPFO website, Unified portal and UMANG app features working fine on one don‘t work same on other.

- Incompleteimplementation documentation of newer features like UPI withdrawals, which are being rolled out to a subset of users, rather than universally.

Assuming it‘s not one of these four thing you are rubbling, then it is anything to do with any of these employers provident fund organisation updates:

My Take After Testing the New Portal for a Week

I probably spent a week going through the new integrated portal flows for claim initiation, update KYC and download passbook. I felt that the these core transactions worked fairly well after login, like checking balance, downloading passbook, updating KYC. The irritating bit was every time you had to go to UMANG for some other transaction; it does not feel like the same product yet.

If you‘re someone who prefers everything to be in one place, my blunt opinion is: It‘s almost there. Mind to be a little patient if you‘re doing a time sensitive transaction (something partial withdrawal for example).

How Employees Can Actually Use These Updates

A few practical moves that make a real difference right now:

- Make sure you Run a Service History check. Make sure all jobs you‘ve done are correctly transferred to your UAN. If not the joint declaration with a current or former employer can set this straight much quicker than making a blind grievance.

- UpdatetheKYC. Aadhaar, PAN, your bank account details and mobile no. should all be consistent in the system for the auto-credited bank transfer and UPI withdrawal to work without hitches.

- MakesmallemergencyUPIwithdrawals, butleave the majority of your corpus compounding there‘s no need to withdraw more than you need when the rate is still 8.25%.

- Download and save your annual passbook after each interest credit… In case of a discrepancy, you will want to have that record to submit through EPFiGMS.

- Have you recentlychanged jobs and havea UAN linkedto Aadhaar? Then see if the transfer happened automatically. You might not have to go through the manual transfer process.

None of that is anything that a financially savvy individual should actually need to do. It‘s more about breaking away from the assumption that the system is correct by default in the first few months.

How Employers Should Handle the New Employees Provident Fund Rules

If you run payroll or HR, the compliance surface became more complex though the basic contribution tree hardly changed:

Makefull use of the amnesty window while itlasts. The 2026 Amnesty Scheme offers a 6 months amnesty window to frtilise PF trusts with a heavy waiver on damages and penalties. In addition, the -employees’ Enrolment Scheme – 2025- provides for an employer to make retroactive enrolment of employees who should have been enrolled from 1st July 17 up to 31st October 2025, with the employee‘s share waived and penalties limited.

Conduct an internal coverage audit today, not after the window closes. Especially if you have contract labour or a complex vendor structure, this is where risks of misclassification tend to lurk.

Reconfirm your definitionof “wages”in your payroll against the text of the EPF Scheme, 2026 as this is a common cause of ECR mismatches which may later attract avoidable penalties.

Observe the Budget 2026 tax changes. For employers, contributions to recognized provident funds are now taxed at a single overall limit of ₹7.5 lakh per annum for PF, superannuation, and similar benefits ahead of the previous combination of percentage limits. Review when designing senior staff remuneration.

If your team manages a sizable sum of KYC and identity data around this process, its probably time to tighten up the storage and delivery of such information too – reading tekysinfo.com‘s article on dodging phishing attacks and account-takeover scams isn‘t a bad place to start, since PF-scouting phishing scams tend to increase every time EPFO makes new headlines like this.

Where to Verify Any of This Yourself

For anything that is time-sensitive – the interest credit date, scheme text, circulars etc. – go to the source. Instead of relying on those one-line summaries on the aggregator sites, check a section called EPFO Updates and Circulars published on EPFO itself. This is the source, where the official scheme data and operational notices are first published, and the best place to check whether a change did actually happen. For those scheme launches specifically, take the newspaper agency‘s release in PIB (Press Information Bureau) called Employees’ Enrolment Scheme. Full details for the eligibility period and conditions are laid out in that in plain government language, without any of the spin that one finds on the aggregator sites.

Frequently Asked Questions

1. Did the EPF interest rate change under the new EPF Scheme, 2026?

No. Still 8.25% for FY 2025–26, credited every year after coming out with official notification for EPFO.

2. What is EPFO 3.0, exactly?

The pooled, digitalised upgraded back end formed by the CITES project one unified database and portal shared by all, no regional IT infrastructure anymore and other features like UPI withdrawals and autopilots.

3. Do I need to do anything because the 1952 scheme is gone?

Not really. You will still get to contribute and/or benefit as before. It‘s good to check your Service History and remember to keep your KYC current when transitioning.

4. What if my employer never enrolled me under EPF?

The Employees’ Enrolment Scheme – 2025 allows employers to backdate for some workers from 1 July 2017 until 31 October 2025 under reduced penalties. get your employer to see whether you are covered.

5. How will I know when this year‘s interest has been credited to my employees provident fund account?

Compare your e-passbook on member portal or UMANG after the announcement by EPF with opening balance, contributions and closing balance to find credited interest.

6. Is UPI-based withdrawal available for everyone?

Only if all your UAN, Aadhaar, bank account & KYC are linked correctly for those withdrawal types that currently support it. The rollout is being done in stages, so sometimes it may be available, when others it isn‘t.

7. How did Budget 2026 affect employer PF contributions?

Consolidated into one uniform ceiling of ₹7.5 lakh / annum, which was previously covered by a sector-wise limit, percentage- based limits, limit on the fund value etc. for employer contributions.

8. Where should I check for the latest official employees provident fund organisation updates?

The best combination is EPFO‘s own Updates and Circulars page, verified against PIB press releases for immediate launches of major schemes.

9. My passbook looks incomplete after the CITES migration should I be worried?

Not right now. Delay due to migration related sync issues are typical at the moment. Wait for couple of days and recheck. If the gap still exists, has to be completed through EPFiGMS raising it with your Service History as backup.

Final Take

The ones being implemented this year at the employees provident fund organisation, is a real infrastructure upgrade, not just a shiny new policy and that is something worth celebrating, despite the flaws along the way. If you are an employee, the changes are straightforward review your Service History, ensure your KYC is up-to-date, and don‘t be alarmed at potential glitches in your passbook during this transition. If you are running payroll, the amnesty and enrolment windows are time sensitive, so best to take advantage of them sooner rather than later.

Is it ripe? Not quite. But we‘ve gotten down the right path, and most of the “friction” people are experiencing is simply a side effect of transitory migration.

Read:

KLR Login Service 137: What It Actually Is

I’m a technology writer with a passion for AI and digital marketing. I create engaging and useful content that bridges the gap between complex technology concepts and digital technologies. My writing makes the process easy and curious. and encourage participation I continue to research innovation and technology. Let’s connect and talk technology!