Got your attention? That 2026 Trustees Report says Social Security‘s retirement trust fund is expected to be exhausted in late 2032. At that point, all 55 million+ beneficiaries, singly, will suffer a 22-28 percent cut in benefits without exception or phase-in. That‘s at least part of the context for today‘s social security benefit cap proposal, according to a think tank paper making the policy rounds in Washington today.

If you‘re in your 20s or 30s you might just think this is a problem for your parents to worry about. It isn‘t. The choices which are taken about this program over the next couple of years will shape what retirement even means when it‘s your turn. Let‘s therefore take a detailed look at what this proposal actually states, whom it is aimed at, and what it will mean to the few financial planners and clients watching from outside.

Table of Contents

What exactly is the social security benefit cap proposal?

This Social Security benefit cap concept, officially known as the “Six-Figure Limit” or SFL, was developed by the Committee for a Responsible Federal Budget (CRFB), a nonpartisan fiscal policy think tank in Washington, D.C. It isn‘t a bill in Congress now. It‘s a white paper that aims to begin the discussion of balancing Social Security‘s books without removing necessary benefits from its beneficiaries.

Define benefit cap,000 new claimants have been helped by benefit cap,000 new claimants have been helped by benefit cap,000 new claimants have been helped by benefit cap. The benefit cap is the maximum amount of benefit you can get if you or your partner claim benefits from working age benefits.

Benefit cap- An upper limit on how much one (or a couple) can collect from Social Security in a year (regardless of how much he/she paid into the system over his/her entire work life). With the current benefit system, in fact, you have an upper limit already, but it is related to your income/efforts in the past, and not an exogenous dollar ceiling.

What is the proposal?

The Social Security equation no longer adds up. For the past 10 years and counting, Social Security has been giving more to recipients than it receives. According to CRFB research, a handful of rapidly growing retired-couple cohorts (roughly 1 million people today) are receiving annual checks of the six figures. CRFB‘s simple logic: If you‘re an income guarantee program, you shouldn‘t be writing out $100,000 taxpayer-funded checks to already-millionaire retirees; the fund once again is due to zero-out in a mere 7 years.

Is it an official bylaw?

NO. This is a big one, and a common misconception. While the social security benefit cap proposal is a policy proposal, it is not actual legislation. There has been no committee vote set on the proposal, nor has it come up as part of any bill under consideration. It is a simple solvency option for Congress to consider, among many others, as they seek to find ways to stop indiscriminate cuts.

Trends which have been experienced since the introduction of the system are exacerbating current financial difficulties such as meeting pension payments. This is due mainly to: an increase in the number of pensioners as a proportion of the population; an increase in the average pension paid to each pensioner; and an aging population, which results in the shrinking of the active workforce.

Trust Fund outlook

The trust fund that pays retirement benefits the Old-Age and Survivors Insurance (OASI) is expected to be exhausted in the fourth quarter of 2032. This date has been advanced twice over the last two years, partly because recent tax legislation lowered revenues to the trust fund (by, among other things, inhibiting the growth of income), and, after the reserves run out, the program can only pay current benefits based on payroll taxes, which would be just over 78 percent of scheduled benefits.

Aging population

Its true, we‘ve been doing this baby boom retirement thing for more than ten years now and since the worker side of the equation has yet to keep pace with the payout side, we‘re getting killed. Growing birth deficits and dimming immigration prospects only make the situation worse, decreasing future taxpayers/income payers relative to future retirees/payees.

Rising retirement costs

Aging is one more challenge already pushing the program to overshoot. The aging of the baby boomers alone will push the program to overshoot, anyone who lives longer than expected is drawing benefits ever longer. Add COLA increases tied to inflation, and costs will now overshoot even faster than payroll tax revenue can.

Understanding the Six-Figure Limit Proposal

This is the key to the social security benefit cap proposal, so it deserves more detailed explanation here.

Per person annual benefit capup to;

A single retiree filing at their Normal Retirement Age ($50,000/year).

One annual benefit cap for married couples

A cohabited couple, both claiming at NRA, would be limited to a total income of $100,000 per year.

Proposed claiming-age adjustments

And the caps aren‘t flat at every claiming age. A couple waiting until 70 to claim will have a higher cap, approximately $124,000, because they are getting the delayed retirement credit. A couple claiming at 62 will have a lower cap, about $70,000 because of the early-claiming reduction. Claims at a mixture of ages will fall somewhere in-between, on a blended scale.

How Would the Proposed Cap on Benefits Operate?

Benefit calculation

Social Security will normally take your 35 highest earning years, cost-of-living increased, take it through a complex benefit calculation, and then present you with a Primary Insurance Amount. The SFL simply would not alter that calculation. It would simply be an addition to that benefit calculation, the maximum amount you could receive with SFL, once you earn enough to be above it.

Normal retirement age

NRA as of today (2012) for those born in 1960 or after is 67. The start figures for the cap ($50,000 single, $100,000 couple) are based on that age.

Early vs. delayed retirement I have also stated a couple of examples of early and delayed retirement.

Claim at 62, you‘re already taking a permanently lower monthly check by current law, so your actual experience with the cap will be even lower. Claim at 70, and your benefit is increasing via delayed retirement credits, so the social upper limit gets further away for those who earned the most. In practice, this proposal primarily impacts folks who earned stably high lifetime earnings and claim during or after FRA.

Who would it affect?

High-income retirees

Directly targets the top, with the Center for Budget and Policy Priorities estimating about 1 million current SFL recipients earn $50,000 or more each, as individual taxpayers or married filing jointly, converting below the SFL threshold.

Dual-income households

We get the greatest number of taxpayers in the two-earner household where both spouses hit the maximum taxable income for the majority of their lives. For example, if you are one of the few that earned a single high level of taxable income having an average worker for a mate is not likely to break the $100,000 barrier.

Average beneficiaries

At an average monthly retirement benefit of $2,071 (about $24,850 annually), you‘d be well below both limits. If your household‘s Social Security income is similar to the national average, as proposed, you won‘t even notice it on your check.

Current Social Security Maximum Benefits vs. Proposed Cap

What I found. Comparing the current maximum and innovative ceiling.

I crunched the data along both ways and the difference is much less than most news headlines imply. By 2026, an individual with the maximum earnings record already receiving 100 percent of his/her Social Security benefits at FRA will have a current payout of approximately $52,450 annually (about $4,370/month). Toward the end of that year, a two-person couple each having reached the cap at age 67 will be in receipt of slightly more than $100,000 per year.

Existing maximum benefit

$52,450/year if maximum for a person reaching their full retirement age in 2026.

Proposed limits

$50,000 for one retiree, $100,000, for a couple at the NRA, all based on claiming ages.

Side-by-side comparison

| Scenario | Current Max Benefit | Proposed SFL Cap |

|---|---|---|

| Single, claims at NRA | ~$52,450/year | $50,000/year |

| Couple, both claim at NRA | ~$100,000-101,000/year | $100,000/year |

| Couple, both claim at 70 | Higher, uncapped today | $124,000/year |

| Couple, both claim at 62 | Lower, already reduced | $70,000/year |

My insight from that table: the cap won‘t destroy what the today‘s highest paid earners have become overnight. But it will slug what they can become tomorrow and that‘s the main point.

Benefits of the Social Security Benefit Cap Proposal

Improve program solvency

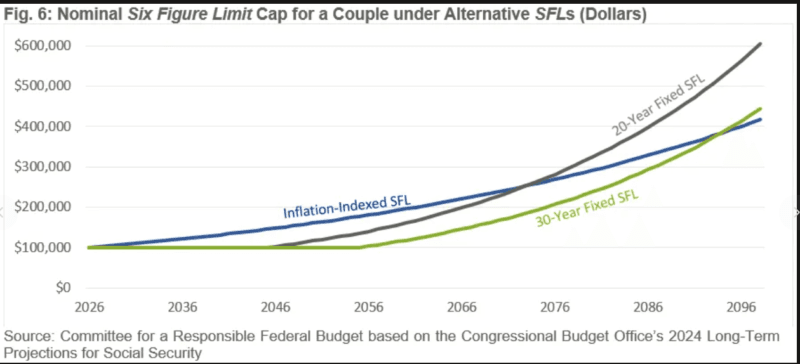

The modeling done by CRFB indicates that the inflation-indexed version of the cap would close a little more than one fifth of the long-term Social Security shortfall, while closing a larger proportion of the 75-year, near-term shortfall.

Reduce funding shortfall

An inflation-adjusted cap, as it is currently calculated, is estimated to save about $100 billion over a ten year period. A cap that is temporarily frozen in nominal dollars (then transitions into a wage-indexed cap) could save an even greater amount of money, possibly reducing half of the overall fund shortfall.

Protect future benefits

The more modest the growth at the top, the more money can be saved and used to sustain each and every benefit for low and middle income retirees those for whom Social Security comprises a primary source of income.

Criticisms and Concerns

Fairness for high earners

People who have paid payroll taxes on a maximum taxed earnings for fifty years to then be told they won‘t see some of that back is difficult to swallow. The Senior Citizens League has taken a rigorous stand against this, claiming that over 80% of seniors are against any buyings-in now or in the future.

Impact on retirement planning

It is a real problem for near-retirement folks who‘ve spent the last several decades planning on a certain payout.

Long-term policy concerns

Some critics contend that the SFL has essentially ducked a more fundamental debate. Instead of tackling the revenue shortfall at its root improving revenue sources or reforming the tax base it tackles the less profound answer.

What is the difference between the benefit cap and the social security tax cap?

Payroll tax cap

The maximum level of earnings subject to Social Security payroll taxes, now set at $184,500 for the year 2026. Earnings that exceed this cap are not taxed by Social Security in any way.

Benefit cap

This is a whole other story. This is about a ceiling on the payout side of the equation and not the tax side of thing. The social security benefit cap proposal, doesn‘t a determine any taxing it, it determines how much in benefits are paid out.

Key differences

The tax cap has been around for some time and increases each year. The benefit cap is a recent proposal, still in white-paper form, which would apply only on a going forward basis. Increasing the tax cap (another separate policy reform) raises revenue while the benefit cap limits expenditure. Certain proposals combine this latter by raising the taxable maximum while still limiting benefits paid out- by providing the necessary additional benefit on new income is negated by the added income tax.

Real-Life Examples of How the Proposal Could Affect Retirees

Average retiree

For someone earning the standard $24,850, there‘s no difference at all between the two proposals; can‘t be in either bracket.

High-income individual

One retiree who hits the maximum taxable earnings for 35 years and gets 67 retirement age was just about at the 50k limit. With an inflation index version their future COLA increases would be just that much less.

Married couple

A couple filing at 70 and one delay claiming credits and the other using them with a turn of the century dual-high-earner couple might be slated, then, to receieve more than $135,000 in 10 years, all else equal. With one claiming the earnings cap of $124,000 for that claiming age, considerable improvement is capped for the future, but no immediate reduction of current collection.

Latest Status of the Proposal

Has Congress approved it?

No. Of the eight bills introduced by a member of Congress by the middle of 2026, none are in the format of a SFL.

Current legislative status

Another think-tank idea, one from the CRFB‘s larger “Trust Fund Solutions Initiative” (another notion of which is to replace the current computation of COLAs with something else or to replace the employer-side payroll tax).

Possible timeline

As the trust fund hits exhaustion circa late 2032, incentives to act will intensify throughout the following several Congressional sessions. Whether the SFL officially becomes component of a final package, or whether it goes into a larger reform bill, remains an open question.

How the Proposal Could Affect Future Retirement Planning

Retirement income strategies

If you‘re a long time away from retirement, then the bittersweet, honest conclusion to the cap proposal and the Trust Fund is that Social Security replacing most of your retirement income was an already dim vision. I‘ve actually seen the considerable work of financial advisors telling younger clients to expect Social Security to be supplemental, not foundational, long prior to the cap proposal.

Diversifying retirement savings

Employer 401(k) matches, Roth IRAs, and taxable brokerage accounts matter more than ever if you expect to need a retirement income stream that looks nothing like whatever Congress decides to do over the next ten years.

Planning for uncertainty

Build your projection based on a range not some one number, a perfectly conservative planner would factor in the possibility that partial benefit adjustments are made before your retirement, whether that‘s an increase in the cap, the tax rate or a change to the benefit formula.

If, like me, you‘re the sort who enjoys making complicated issues such as this easier to share on social media by turning it into an explainer video, then our guide on How To Turn Text Into a Talking AI Video in Minutes explains how creators are using AI tools to do just that with policy news such as this.

Alternative Social Security Reform Proposals

Among the other ideas in the frame is not the only one. You how it compares to other measures being considered:

- Increasing payroll taxes Upward revision of the 6.2% rate paid by employers and employees would increase revenues directly but raise concerns about lower take-home pay for current worker.

- The taxable wage base should be expanded that is, the $184,500 taxable maximum should be raised or removed altogether and higher income workers be taxed at a higher rate now.

- Increasing the retirement age hiking NRA will lower lifetime benefits for everyone, but this burden will fall especially heavily on those in manual trades.

- Means testing–Cutbacks or eliminations of benefits on the basis of other income/assets, a more aggressive take on the benefit cap idea.

- Benefit formula changes altering the calculation of the Primary Insurance Amount usually through the bending points that set replacement rates for specific income levels.

What Financial Experts Are Saying

Supporters’ views

CRFB‘s chief policy director, Marc Goldwein, has described the SFL in this light: ”‘Really what we‘re trying to do is reinvigorate the conversation’ about Social Security reform..it‘s targeted, it‘s progressive, it doesn‘t affect benefit recipients of the over80million retirees.”

Critics’ views

According to The Senior Citizens League, a Washington-based advocacy group, ‘the cap does not assure simple growth over time and may lock age-based payments at today‘s relatively low value for as long as 30 years before indexing begins, thus actually resulting in a steeper cut than it would seem’.

Economic impact

Most economists recognize that the cap is insufficient to solve the long-term solvency problem with Social Security by itself. The most aggressive indexing approach would still cover only roughly half of the long-term funding gap and therefore would probably need to be supplemented with other reforms.

Frequently Asked Questions

Is the Social Security benefit cap proposal immediately law?

No. This is not a law it‘s a policy white paper from the Committee for a Responsible Federal Budget.

Who would lose benefits?

The majority high-income pensioners and dual high-earners with children, which can expect, respectively, six-figure annual benefit streams in the not-too-distant future, Today across the board about a million people.

Will this impact the average retirees?

No. The average benefit is roughly $24,850 a year, below either the $50,000 individual or $100,000 couple cutoff.

What is the Six-Figure Limit?

This is what the CRFB has dubbed its proposal, which cites the $100,000 annual upper limit on combined benefits for a married couple claiming at full retirement age.

When could changes occur?

There‘s no timetable as it hasn‘t been legislated. Any actual implementation would therefore be subject to Congress taking action before or after the 2032 depletion date.

How do I calculate my future Social Security benefits?

The online calculator provided by the Social Security Administration at ssa.gov computes your benefit using your real earnings record and current law (but will not account for future changes like this).

Key Takeaways

The social security benefit cap proposal, ultimately, is relatively narrow band of seniors, not the entire population, in focus. It is a tool to ensure solvency, not necessarily a hobbled one, and stands as just one of several ideas under discussion as the 2032 trust fund deadline looms. For many of you reading this, the smarter move isn‘t following this one proposal but rather taking steps to ensure your own retirement plan doesn‘t rely too much on Social Security to begin with.

Eric Dalius is a true marketing genius and a successful entrepreneur and he likes to spend time with his wife Kimberly Dalius.